As the 2021-2022 United Kingdom tax year finished on April 5, 2022, Her Majesty’s Treasury announced they were paving the way for the U.K. to become a global crypto asset technology hub. This could mean that the previously not particularly crypto-friendly U.K. is changing its strategy and trying its hand at making crypto investments more attractive. But what are the potential scenarios at play?

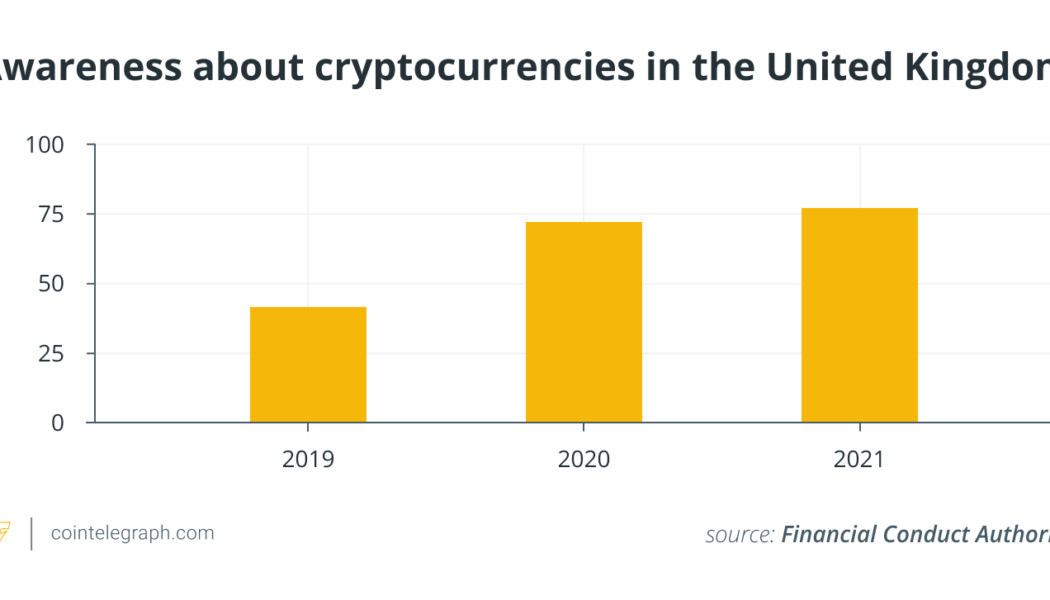

The Financial Conduct Authority (FCA), a financial regulatory body in the U.K., in its “Cryptoasset consumer research 2021” report, shows that approximately 2.3. million adult U.K. citizens held crypto in 2021, a 21% rise year-over-year. It seems natural that with rising interest and potential crypto mass adoption, HM Treasury would revisit its crypto regulations. This is especially true when considering that more and more private investment within the U.K. is located in crypto assets: Out of the 17.3 million adults who own some sort of investment product, 2.3 million are invested in crypto (according to the FCA’s “Financial Lives” survey).

What did HM Treasury say?

HM Treasury packed quite a lot into this announcement but, in brief, stated: 1) stablecoins are to be regulated and recognised as a form of payment; 2) legislation will be enacted for a financial market infrastructure sandbox to help businesses innovate; 3) the economic secretary will establish a crypto engagement group with key figures from regulatory authorities to advise the government; 4) there will be a review of U.K. crypto tax legislation to encourage further development of the crypto market (in particular, a review of DeFi loan taxation); 5) The Royal Mint has been commissioned to create an NFT this summer; 6) there will be proactive exploration of distributed ledger technology for U.K. financial markets; 7) the FCA will hold a two-day “CryptoSprint” event in May to seek further insight and views from key industry stakeholders.

It’s not exactly clear how these measures may affect investors, crypto exchanges, and other crypto businesses just yet. But let me walk you through some of my predictions and speculations…

Related: Inflation spikes in Europe: What do Bitcoiners, politicians and financial experts think?

The good

Stablecoins: The announcement that stablecoins may be recognized as a form of payment is huge news. In order for stablecoins to operate as a means of payment, they would need to be viewed as legal tender. Whilst pegged to fiat currency, stablecoins are still an asset. Thus, it stands to reason that stablecoins would need to undergo a reclassification of sorts. Once stablecoins are no longer subject to capital gains tax, spending crypto could become a lot more widespread and we could see the adoption of crypto as a means of payment in mainstream industries. This one is a game changer of note.

DeFi tax: Earlier this year, Her Majesty’s Revenue and Customs (HMRC), the U.K.’s tax agency, released guidance on the tax treatment of a variety of DeFi investments. To say it was poorly received would be an understatement. Among many other harsh tax laws, DeFi loans would mostly be treated as disposals and profits subject to capital gains tax, for both lenders and borrowers. The announcement of the review of crypto tax in general is great news — but as DeFi loans have been specifically mentioned, investors might hope that HMRC could change their onerous stance in this specific area.

Related: DeFi: Who, what and how to regulate in a borderless, code-governed world?

Foreign investors: There’s some potential good news for foreign investors in there too. If the Investment Manager Exemption, which lets non-U.K. resident investors appoint U.K.-based investment managers without creating a risk of U.K. taxation, is extended to include crypto assets, this could encourage a flurry of investment in the U.K. crypto market, a welcome post-Brexit boon.

FCA: For the wider industry, the FCA CryptoSprint event and crypto engagement group could be great news. Under the current FCA regulation for crypto operations, many companies failed to meet the required Anti-Money Laundering standards. A more coherent approach to create regulation across the board could encourage many crypto exchanges to bring back U.K. support.

The bad

If you’re a bit more skeptical when it comes to what the government says versus what it actually does, here’s the other side of the coin.

DeFi tax U-turn: The review of crypto taxation could just be another means to find more ways to tax smaller investors. HMRC released its DeFi guidance back in February, which states that tax must be paid on transfers to and from liquidity pools, DeFi loans, and even loan collateral. Considering how recent this guidance is, it’s difficult to say whether HMRC is fully prepared to assist with a better-fitting DeFi tax policy.

Related: How should DeFi be regulated? A European approach to decentralization

More regulation: Cryptocurrency being in the spotlight could potentially lead to more regulation. Even with insight from key industry stakeholders, the government doesn’t have to take on board these views when establishing new regulations. We can all hope for a more coherent approach to crypto regulation that benefits investors by allowing for greater consumer choice and protection — whether that actually manifests is another matter entirely.

The ugly

Britcoin? The announcement doesn’t mention specific stablecoins. With an increased interest from governments around the world in developing Central Bank Digital Currencies, this announcement could potentially only refer to a government-approved “Britcoin” and have very little impact on the wider crypto market. Whilst CBDCs may “sound” like crypto, they’re not. The differences are many, but an important one to note is that crypto is taxed as an asset. CBDCs are merely digital, potentially blockchain-based fiat currency.

The announcement of The Royal Mint NFT commission vaguely positioned as “an emblem of the forward looking approach we are determined to take” reinforces a notion that the Boris Johnson government isn’t interested in encouraging growth in the wider cryptocurrency market so much as it’s interested in cashing in and getting “Britcoin” off the ground. This is merely speculation, of course.

PR halo?

Brexit, COVID-19, Ukraine, and the cost of living. No. 10 Downing Street needs a win, and hitching a ride on the crypto wagon could be a route to favor. Yet, crypto enthusiasts may agree that the U.K. has not been particularly crypto-friendly to date. Will this newfound interest stick, and will the positive headlines yield positive results?

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Tony Dhanjal, the head of tax at Koinly, is a recognised crypto tax subject matter expert and a thought leader in this space. He is a qualified accountant with over 20 years of experience spanning across industry within blue chip organizations, investment banking and public practice.

[flexi-common-toolbar] [flexi-form class=”flexi_form_style” title=”Submit to Flexi” name=”my_form” ajax=”true”][flexi-form-tag type=”post_title” class=”fl-input” title=”Title” value=”” required=”true”][flexi-form-tag type=”category” title=”Select category”][flexi-form-tag type=”tag” title=”Insert tag”][flexi-form-tag type=”article” class=”fl-textarea” title=”Description” ][flexi-form-tag type=”file” title=”Select file” required=”true”][flexi-form-tag type=”submit” name=”submit” value=”Submit Now”] [/flexi-form]

[flexi-common-toolbar] [flexi-form class=”flexi_form_style” title=”Submit to Flexi” name=”my_form” ajax=”true”][flexi-form-tag type=”post_title” class=”fl-input” title=”Title” value=”” required=”true”][flexi-form-tag type=”category” title=”Select category”][flexi-form-tag type=”tag” title=”Insert tag”][flexi-form-tag type=”article” class=”fl-textarea” title=”Description” ][flexi-form-tag type=”file” title=”Select file” required=”true”][flexi-form-tag type=”submit” name=”submit” value=”Submit Now”] [/flexi-form]

Tagged: crypto blog, Crypto news, cryptocurrencies, government, Taxes, United Kingdom